The recovery of a “money economy” in late medieval Europe was attended by two other developments which were missing from the “money economy” of the ancient world:

1) a greatly refined paper making process, and

2) the invention of the printing press.

The impact of paper and the printing press has been felt in economics nearly as much as it has in publishing. The phrase “paper money” is a subtle contradiction of

terms. It was noted that “money” strictly defined is gold and silver in coin form. Nothing that is made out of paper can qualify as money. Another question is: can paper serve the same purpose as money? There is some intrigue in this notion that has resulted in attempts to circulate paper instead of money ever since it was mechanically possible to do so. Hans Sennholz explains,

“…the universal use of paper monies today was made possible only by their prior use as substitutes for real money, such as gold and silver, for which there was an industrial demand. Only when men grew accustomed to these substitutes, and governments deprived them of their freedom to employ gold and silver as media of exchange, did paper emerge as the only exchange medium.”

Advocates of “paper money” persist in modern times. For the most part, they indulge in the fantasy that “money” functions merely as a token, and does not need to possess any “intrinsic value”, As a first step in understanding the economic changes in the dawning of the modern era, some modern misunderstandings about

the history of money shall be examined. Two cases in point are theories concerning the clay tablets of ancient Babylon and the “tally sticks” of medieval England.

Ancient Babylon, “the earthly city”, made extensive use of clay tablets for the purpose of recording contracts and debts. The function of these clay tablets was much the same as modern-day checks and promissory notes. In fact one historian has said, “Babylonia was thus the motherland of our modern commercial usages and commercial paper.”

_______________

Hans Sennholz, Age of Inflation (Belmont: Western Islands, 1979) p. 14

H.E. Barnes, An Economic History of the Western World (New York:Harcourt,

Brace & Co., 1942), p.25

While it perhaps is true that in concept paper money-substitutes are begotten of Babylonian economics, it also is the case that in Babylonia clay tablets were record-keeping devices, and did not circulate as exchange media. A modern writer, RK. Hoskins, goes too far when he remarks concerning Babylonian banks, “These banks offered almost every service offered by banks today including the use of checking, savings, letters of credit, and the Babylonian form of paper money – the clay tablet. The banks kept the gold – naturally.” In the first place, Babylonia had a silver based economy, not gold. Secondly, while the clay tablets serviced all of

the banking functions that Hoskins lists; they were not used as money.

Ancient men came by their goods with much difficulty. Production techniques were burdensome, and the transportation of goods was dangerous. An ancient man would not give real goods in exchange for someone’s promise to pay him later, recorded on a clay tablet, unless he consciously was giving the other a loan.

Another misunderstanding of history that is used to promote “paper money” involves the “tally sticks” of medieval England. These were wooden sticks that were notched along one side and split lengthwise. One half was kept in the royal treasury and the other in private hands. Since the notches on both halves were to match, there was little likelihood that the data encoded on the sticks could be corrupted. What was the function of these tally sticks? Thoren and Warner, in The Truth in Money Book make a preposterous suggestion. They claim, “Tally sticks were used exclusively as money in England for 594 years” (supposedly beginning with Henry the First in 1100). The fact of the matter is that English kings steadily issued a silver coinage since the recovery of a “money economy” after the fall of Rome. For a full account of such coinage see John Kent’s 2000 Years of British Coins and Medals. Cunningham explains the actual function of the tally sticks. The county sheriffs were accountable to collect taxes in their areas and make payment of them to the king. Taxes were payable in two installments, at Easter and Michaelmas (September 29th). “… at Easter the sheriff made a payment on account, of half the sum due in the course of the year; this was credited to him, and he received a tally as a voucher. At Michaelmas he had to render his accounts in

_________________

. Hoskins,War Cycles – Peace Cycles (Lynchburg: The Virginia Publishing Co.,

1985), p.6

C.A. Herrick. Ph.D .• History of Commerce and Industry (New York: Macmillan

Co., 1920), p.32-34

e.g. Thoren & Warner, The Truth in Money Book (Chagrin Falls: Truth in

Money, inc., 1984) p. 228

British Museum Publications, 1978

due form … The first item taken was the sum which had been paid into the Exchequer at the previous Easter, and for this a tally was produced. ” As is evident, the tally sticks of medieval England functioned in much the same manner as the clay tablets of Babylonia. They did not support the range of banking activity as did the clay tablets, however, they functioned similarly as record keeping devices. The sheriff did not pay taxes with tally sticks; he furnished tally sticks as a statement of a previous partial payment of taxes in silver. They did not circulate as money; and there is absolutely no warrant for the claim that, “Tally sticks were used exclusively as money in England for 594 years.”

Neither Babylonian clay tablets nor medieval English tally sticks were early versions of “paper money”. “Paper money” evolved from the ancient and medieval use of various substances to represent a debt of money, such as the tablets and the sticks. The critical stage of the development of “paper money” was the use of paper to represent, not a claim to money, but the money itself. Once this practice gained

popularity, there was little complaint when the modern feature appeared, viz. the use of paper as money itself instead of silver and gold coin. This process of evolution is fairly subtle, and deserves some elaboration, for the onset of “paper money” in modern times has served to provide the “bite” of usury with a seemingly innocuous mask. “Paper money” has tended to slow the inevitable upheaval that usury causes in a society, because, as usurers absorbed too much of the available “money”, more could be printed. In order more fully to understand the dangers of this false solution, its origins must be considered.

The use of paper to record debts greatly expanded in the late medieval and early modern eras, along with greatly expanding trade and newly emerging industry. Levels of wealth in silver and gold were beginning to be amassed such as was not seen since ancient times. But the advantages of these media as a store of wealth also presented a new problem of security. Not only could great wealth reside in a relatively small place in the form of silver and gold coins, but as well, great wealth

could fairly easily be stolen in the form of silver and gold coins. Not only did these exchange media provide a convenience to the merchant, but to the thief also. Metal smiths, who’s livelihood involved large quantities of silver and gold. had installed security measures such as vaults. It happened that those who had a security problem with their money made arrangements with metal smiths so that the smiths would store the money in their vaults. Of course a receipt was issued entitling the owner to the correct ‘quantity of money. This receipt was the basic paper record of

______________

Wm. Cunningham, The Growth of English Industry and Commerce (1910; New

York: A.M. Kelly, 1968), Vol. I, p.156,157

a claim to money.

Another type of this paper record was the “bill of exchange”. As commerce spread over greater and greater distances, it began to encompass not only all of Europe, but to reach beyond the Mediterranean Sea and the Atlantic Ocean. The shipment of goods over these distances still was hazardous, but not to the extent as the shipment of silver and gold. In order to alleviate the problem of shipping large quantities of silver or gold, merchants began to accept “bills of exchange” instead of immediate payment for their goods. These bills entitled them to payment of the correct sum through one of the buyer’s associates in a location that was closer to home for the merchant. In this transaction, one party would give up goods and in return he would receive but a piece of paper. This sort of thing was unthinkable in earlier centuries due to the lack of any certainty whatever that the promise to pay ever would be made good. It became thinkable to receive paper in return for goods only by the organization of the metal smiths into larger and internationally associated banks. The utility of the bill of exchange depended on the confidence of the participants in the system. Lacking the confidence that a bill could be redeemed for money, a merchant hardly would accept one in exchange for goods.

Actually, such an arrangement was not an exchange. It was the initiation of an exchange, but the exchange would not be complete until the bill was redeemed for money_ Once the buyer has his goods and the seller has his money, and only then, could it be said that there was an exchange. That may sound like an irrelevant technicality, however, the reader must remember his own context. The late 20th century man does not view paper “money” as a contract or a promissory note. As its appellation implies, it is viewed as if it were itself money. However, the medieval and early modern merchant had no such concept. For him the value of the bill of exchange lay in its promise of a future payment of money (silver or gold coin).

The convenience of receipts for deposit of money and bills of exchange served to reveal other inconveniences. Both the receipts and the bills entitled a particular person to a particular sum of money. But, if one had the confidence to hold paper for a time to represent his claim on money, he could expect that those with whom he dealt also would be willing to do so, and in most cases it was likely that they already were doing so in the matter of their own personal accounts. So, in making a

purchase locally, why not simply sign over one’s receipt for money to the seller, instead of getting the money out of the vault, handing it over to the seller, and him turning around and depositing it back into the vault under his name? Or, in the case of bills of exchange, would it not be advantageous if they were useful in the course of one’s journey – to be exchanged for goods in the same manner in which one originally had received them? The problem to be overcome was the constant noting and dating each use of the paper in exchange, in order to identify the new payee. Certain changes in the makeup of the paper were needed in order to make them more suitable for this purpose. First, they had to be made anonymous, entitling whomever had them in their possession to the money which they claimed. Secondly, they had to refer to standard denominations of money instead of a particular account balance or the price of a particular sale. In this way, various combinations of the bills could better serve transactions of any amount. These changes greatly facilitated trade, however, they also made for a subtle change in the nature of bank paper. Now, instead of bank paper representing the claim of a particular person for a specific quantity of money, it now represents the money itself. If money, in standard denominated units, was payable on demand to whomever held a piece of paper which represented it, then once again a convenience for trade proves also to be a convenience for the thief. The reason that the silver and gold is in the vaults is in order to secure it from thieves. If pieces of paper are out in general circulation, which represent the silver and gold, and which carry the commitment to pay the silver and gold, on demand, to whomever has the paper in his hand, then the security problem is presented all over again. Now a vault is needed in which one may secure his anonymous paper receipts and bills

from thieves.

The entrance of banks into the exchange of goods by providing redeemable paper signals the beginnings of an economy of questionable merit. It already was noticed that it is the pragmatic inhabitant of Babylon, “the earthly city”, who will disregard what ought to be done in favor of what can be done. Each step in the evolution of “paper money” was dictated by convenience. Convenience surely is a legitimate consideration in one’s contemplation of a course of action, but it ought not to be made in his mind the ultimate standard of value. Men ought rather to prove themselves to be citizens of “The City of God”, who “take every thought captive to the obedience of Christ:’ (II Corinthians 10:5). They must weigh the overwhelming inconvenience of transgressing the law of God more heavily than anything else. Banking practices based on redeemable paper are not sinful in themselves. But,

1) they quickly turn into banking practices based in irredeemable paper, which shall be discussed in turn, and

2) while not in violation of the law, they do run counter to the counsel of God, which shall be discussed presently.

Repeatedly the Wisdom (Proverbs 6:1; 11:15; 17:18; 20:16; 27:13)

warns about the dangers of “going surety”. “Surety” is sharing responsibility with another for a debt. Contemporary Christian financial

counselors appeal to the Proverbs which warn of surety as a basis for warning against co-signing for a loan. This is sound advice, however, it does not cover all instances of surety. If a buyer owes a seller some money in exchange for goods, and if he presents to the seller a bill of exchange, in essence the buyer and the banker have entered into a surety arrangement together to pay the money. If the bank for some reason does not pay the money, the seller may still require it of the buyer. If the bill is not presented for payment, but is passed on to yet another seller in exchange for goods. the surety for payment passes to the new buyer. With the changes in bank paper described above, paper began to circulate as a medium of exchange. Banking became a clearing house operation. Banks would track the credits and debits of each transaction involving their paper, and only periodically make actual money payments to settle accounts. Such a system was not strictly unlawful, but inasmuch as it was based on surety, it manifestly was not a good idea.

The inadvisability of the circulation of bank paper as a substitute for money was further indicated by the fact that it quickly reverted to schemes that blatantly were unlawful. Yet these schemes were nothing new, they merely were a new way of committing the ancient sins of inflation and usury. The reader will recall that in ancient times rulers inflated their currency by a process of “debasement”. They could mint more coins than before because they put less silver into each one, so the

silver went further. Banks in the early modern era accomplished the same thing by issuing receipts promising to pay a greater quantity of money than they actually had in their vaults. As the paper itself began to be accepted as media in exchanges, it was noticed that the great majority of the precious metals was allowed to rest in the vaults. The paper representatives were out doing the job of money, so there was little demand for the silver or gold itself. The paper still certified that a certain

amount of money was payable on demand to the bearer of the paper, but it was difficult not to notice that most of the people most of the time were content not to demand it. Banks easily could carry on their functions with only a fraction of the silver and gold in the vaults. Although it never would have entered the mind of a righteous man, however, this meant that

1) some of the metal could be loaned out at usury and not be missed, and

2) more paper could be printed and loaned out at usury. The former was tempting in the case of international loans and usury; the latter in the case of domestic loans

____________

e.g. Larry Burkett, Your Finances in Changing Times (Chicago: Moody Press,

1982)

and usury. Inflation by means of the printing press proved to be a help and a hindrance to usury. It was a help in the sense that the stock of paper in which the loans were payable was less obviously finite in dimension than silver or gold. If usury was close to absorbing all of the paper, more could be printed to keep the usury payments flowing, and thus the social unrest that attends wide spread defaults could be postponed. The hinderance to usury was that continuously inflating the supply of paper in such a manner is ruinous of the economy, because the exchange value of the paper is eaten away. The usury continues, but the paper in which it is paid is less and less valuable. Usurers complain about inflation, and adjust the level of usury to compensate for the devaluation of paper, but on the whole it seems that they are willing to trade a little loss of value for a gain of social stability. Of course, the stability is only illusory, because inflation itself is de-stabilizing, since it eventually ruins the economy. The semblance of stability actually is only the delay of the “day of reckoning”. The illusion of social stability that comes by way of unrighteous manipulation is but the storing up of wrath for a day of even more severe judgment.

There remained one last obstacle to the solidification of this inflate-and-lend approach to usury in modern banking. If the paper lost too much value through inflation, people would choose not to use it because the declining value of the paper would tend to neutralize the convenience of the paper. What was needed was a means of protecting the “investment” of inflating paper, so that there was some assurance that when it came back with usury it still could be “spent” for real goods. This problem was solved by the arbitrary decree of governments, who by this point were surviving on bank loans, and had a vested interest in the solution of the problem. Their answer was “legal tender” laws. The idea basically was a government decree that certain privileged bank paper was declared to be money, and must be accepted if it is offered in payment of debts, “public and private”. This, of course was a gross loss of freedom, and an unrighteousness in itself. The British financier, Sir Thomas Gresham, observed that “Bad money drives good money out of circulation”, (Gresham’s Law). That is, if paper will circulate as money, and do the job of money, then why spend money? Lately, Hans Sennholz has pointed out that “legal tender” laws are the power behind Gresham’s Law, and that if people were free to enter into exchanges with whatever they wanted to use, then paper would not be accepted and Gresham’s Law would operate in reverse: money would drive paper out of circulation.

_____________

Sennholz, Money and Freedom (Cedar Falls: Center for Futures Education, Inc.,

1985)

Modern banking may be considered as commencing in 1694, with the establishment of The Bank of England. This bank was given a charter by Parliament to issue paper notes (over and above the stock of money) to be loaned to the government and to commerce upon usury. Fourteen years after the bank was chartered, Parliament granted to it an exclusive monopoly on the issue of notes. In 1797, the Bank of England suspended the payment of money for its notes. The problem was a lack of silver and gold, or, looked at another way, too much paper. England has no silver or gold mines, and always has relied on international conquest or commerce for the influx of the metals into the land. Since the bank was pursuing an inflationary course, it had extended many more pounds in paper notes than it had pounds sterling of silver with which to pay them. All seemingly was well as long as people generally were content to hold and trade paper, but a threat of invasion by France stimulated the general population to desire money instead of paper. From there, the bank’s notes traversed a steady course of depreciation. No longer payable in money, all restraint on the quantity of issue of the notes was gone. There was a plan devised for the resumption of the redemption of notes in money, but it could not reverse the ill effects of the inflation of paper because it involved the arbitrary government control of the price of the precious

metals. Governments cannot create value, and therefore cannot effectively control prices. The outcome in this case was a change of the Bank’s charter in 1833, declaring its notes to be “legal tender”.

The printing of a piece of paper that is denominated in some weight of silver, and pretends to be payable in silver on demand, when in fact there is no silver that is dedicated to the redemption of that paper, is rightly to be considered the creation of money out of nothing. The principle may seem alarming to one who is beginning to understand it for the first time, but it was rather frankly and bluntly stated by William Paterson in 1694, upon obtaining the charter for the Bank of England, “The Bank hath benefit of interest on all moneys which it creates out of nothing.” This is the startling feature of the course of usury in modern times. Heretofore, some work or labor was required in order to generate something to be loaned. Granted, it usually was not the sweat of the usurer that provided him with excess to loan, but the usury paid to him came from some one’s productive efforts. Now, the initial principal of a loan of “money” comes from nowhere. The moment before the loan was granted, the “money” did not exist. Whether by means of printing some bank notes, or by the even subtler means of simply crediting the borrower’s

_________________

see G. Tucker, The Theory of Money and Banks Investigated (1839; New York: Greenwood Press: NY 1968), p.333-340

cited in Carroll Quigley, Tragedy and Hope (New York: Macmillan Co., 1966), p.49

account, the banker, by the stroke of his pen, brings into being what the legal tender laws say that merchants must receive in exchange for their goods. The borrower has no privilege from the state to create “money” out of nothing. The paper with which he will repay the loan must be acquired by means of the sweat of his brow, and that with usury as well. There is an injustice inherent in one loaning solely by means of one’s wrist reflex what another must repay by means of sweat. On top of that, the one who sweats must repay a greater quantity of what the banker created. But the banker did not create enough for the borrower to repay

with usury; he only created enough to make the loan. The borrower still can repay his loan with usury, if the velocity of circulation is high enough, that is, if money changes hands fast enough, but velocity of circulation cannot increase indefinitely. Eventually there will be defaults and foreclosures.

This problem was painfully evident in the ancient world, but the modern employment of paper served to obscure the threat of usury on the economy. By the nineteenth century, usury was a non-issue among the new breed of economists, Adam Smith, who may be considered the father of modern economics, did not devote so much as a paragraph to the defense of usury in his very large work, The Wealth of Nations (1776). The controversy over usury had engaged thinking men for centuries, and had spawned thousands of pages of debate, yet consider the ease with which Smith dismissed the issue. He simply observes: “In some countries the interest of money has been prohibited by law. But as something can every-where be made by the use of money, something ought every-where to be paid for the use of it.” That is it. He provides no analysis of the biblical texts, the ancient philosophers, the church fathers, or the scholastics. The indication is that Smith considered the opposition to usury to be so unworthy as to merit not even an argument. All opposition is set aside merely on the basis of the instinct of covetousness. If someone gains from a loan, then the covetous lender is not satisfied to receive back only what was loaned. Rather than feeling blessed because the borrower taught him a profitable way to employ his goods, the covetous lender would attempt to justify a claim on the borrower’s goods. When covetous men stand to gain much through little or no work, almost anything can be justified in their minds.

It was this wide-spread dismissal of opposition to usury that provided the appropriate ideological context for the “national bank”. “Usury” now was

_______________

Adam Smith, The Wealth of Nations (Cannan edition, New York: Random House, 1937), p.339

understood to mean “excessive interest”, and now “usury laws” no longer prohibit interest taking plain and simple, but restrict interest taking to an arbitrary statutory limit. Only the near-sighted could interpret this as economic progress. The heritage of Western Christendom is the plain and simple prohibition of usury. The regulation of usury is nothing but a reversion to the ancient course of Babylon. True progress is defined in terms of the ideals of God’s word. Europe,

however, abandoned the quest for the “City of God”, and followed covetousness into the mire of the “earthly city”. The abandonment of the biblical idea of usury, together with the irredeemable “paper money” ploy, allowed the “national bank” idea to be pursued with great vigor. Paper, which could be printed at will, promised to solve the problem of usurers absorbing all the money. But the appetite which usury incites is insatiable. The more “money” that exists, the more there is to be absorbed through usury. The day of reckoning may be postponed by various means, but it cannot entirely be evaded. This was experienced in the extreme by France at about this same time. Tucker’s summation of their fiasco is enlightening:

The first bank of circulation in France was established two-and-twenty years after the bank of England; and, though it lived little more than four years, it became more memorable than any other, from its connection with the most extensive and ruinous scheme of speculation which history records. This bank, which has given celebrity to its founder, – John Law, a Scotchman, – was established in 1716, under the auspices of the duke of Orleans, then regent of France, for the express purpose, as some suppose, of Wholly or partially paying off the public debt, – then amounting to 2,000,000,000 of livres, and of which the government was unable to pay the interest.

Law’s paper program failed because Gresham’s Law began to operate once the bank notes were given legal tender status. The paper suffered a series of depreciations, and there finally resulted wide discontentment over losses due to inflation. Though this was not the sole factor involved, still the debt, which usury had made great and unpayable, figured prominently in the onset of the French Revolution.

Meanwhile, in colonial America, the ravages of the dishonest weights and measures known as inflation was once again demonstrated. England was having her own problems of scarcity of money (overabundance of paper), as was seen above. It was decreed a criminal offense to ship any British coins to the colonies.

___________

13.Tucker, p. 343

What precious little money the colonies were able to accumulate by trade served as a basis for their own monetary system. It was impractical for the coinage to serve as the totality of their currency, so once again men turned to the printing press. However, the various colonies adopted various ratios of value for their paper vis-a-vis the pound sterling. Trading between the various colonies’ paper was exceedingly complex and a breeding ground for fraud.

Since the colonies originally were populated by Puritains and separatists, a strong anti-usury sentiment was ingrained from the beginning. For example, William Penn, a separatist and founder of the state of Pennsylvania, said, “Interest has the security, though not the virtue of a principle. As the world goes it is the surer side; for men daily leave both relations and religion to follow it.” However, the pressure that earlier was felt in England, to allow some usury in order to stimulate trade, also was brought to bear in the colonies. Usury was tolerated under the trade and commerce justification, was regulated under the laws, and was fueled by the paper money fires.

Debts mounted as the value of the paper currency fell. The calamities of debt and paper money were a large part of the obstacle faced by the colonies in their fight for independence. In a letter of December 21, 1776, Robert Morris, a signer of the Declaration of Independence, said of the trials endured by the colonies, “I must add to this gloomy picture one circumstance, more distressing than all the rest, because it threatens instant and total ruin to the American cause, unless some radical cure is

applied, and that speedily; I mean the depreciation of the Continental currency.” As is well known, the military exploits of our founding fathers turned from gloomy to victorious. However, the monetary problems were worsening. A letter writer from Delaware, September 2, 1777, declared, “.. .it is my fixed opinion that America has much more to fear from the effects of the large quantities of paper money than from the operations of Howe and all the British generals.”

The nature of the problem with the colonial paper and the Continental Currency was obvious to thinking men. One such man, Roger Sherman, provided a lengthy commentary on this problem in his, A Caveat Against Injustice, subtitled, An Enquiry into the evil Consequences of a Fluctuating Medium of Exchange.

_____________

Penn, Some Fruits of Solitude, §152

cited in Commanger & Morris, eds. The Spirit of ‘Seventy- Six (New York:

Bonanza Books, 1983), p. 789

IBID, p.791

Originally published in 1752, his treatise dealt with the legal tender laws of the colony of Connecticut. He said, “If what is used as a Medium of Exchange is fluctuating in its value it is no better than unjust weights and measures, both which are condemned by the Laws of God and man, and therefore the longest and most universal custom could never make the use of such a Medium either lawful or reasonable.” The destruction and poverty suffered in the colonies under the inflation of paper served to yield considerable support for the anti-paper view. Also prominent in causing the push to reform the new nation’s monetary situation was the mass of debt which burdened the states following the war. Madison’s statements of accounts as of 1783, show a total public debt in excess of 36 million dollars. Usury on this debt had by that time accumulated to $2,362,320.18

In framing our present Constitution, the Continental Congress acted to solve the inflation problem. Article I lists the duties of Congress, and in Section 8 is included, “To coin Money, regulate the value thereof, and of foreign Coin, and fix the Standard of Weights and Measures.” It is difficult to consider the printing of paper as the “coining” of money. This provision clearly seems to authorize Congress to provide for the minting of silver and gold coins. In addition, the final Section of Article I limits the rights of the States in certain matters. At the insistence of Roger Sherman, there was included, “No State shall … make any Thing but gold and silver Coin a Tender in Payment of Debts.” In keeping with the duties of Congress, the term “dollar” was defined in the coinage act of 1792, as

being 371.25 grains of silver. This was based on the specifications of the Spanish Milled Dollar, or Piece of Eight, which had become well known allover the world by that time. The term “dollar” was derived from the German “thaler” (pronounced “taller”), and always has denoted a certain weight of silver. There was all the appearance that America was on her way to monetary reform.

However, certain influential men remained in the new government who were very vocal in their desire for a Bank of America after the pattern of the Bank of England. Alexander Hamilton was one of their ranks. He became Secretary of the Treasury under Washington, and in 1791, succeeded in his efforts to secure a charter for America’s first national bank. Its charter was for twenty years, and in 1811, was allowed. to expire. It has been suggested, and indeed there is considerable evidence, that the War of 1812, was brought upon this country as a

_____________

reprinted by Spencer Judd: Sewanee, TN 1982

The Spirit of ‘Seventy-Six, p.788

means of tempting Congress to renew the bank’s charter in order more conveniently to finance the war.

International bankers were (and are) a close fraternity. The “inflate-and-

lend” scheme of banking and usury does not admit numerous competitors, for this approach tends to accrue all wealth to the hands of the few. The Rothschild family stands out in history as a prime example of the manipulating power of international banking. Sons of the patriarch Rothschild spread their banking network across Europe, setting up shop in Germany, Austria, England, France, and Italy. By means of usury on an international scale, they were able to consolidate great wealth and power to turn world affairs according to their own fancy. It certainly was not out of the question for them to further their own name and wealth by any means at their disposal, including war. The existence of a national bank in America, with a monopoly on the issue of interest-bearing paper that is declared by the government to be “legal tender”, is according to the program of international banking. It is not unthinkable that war would be a devise for securing the reality of such a bank. Whether or not by human design, it was the effect of the war of 1812, that in 1816, a Second National Bank was chartered, also with a twenty year charter. In the course of its existence, it created tens of millions of “dollars” out of paper and ink, and loaned them out at usury, mainly to the government.

Usury under the paper money scheme creates social turbulence in the same way as it did under silver and gold in the ancient money economy, with one important difference. In ancient times, the misery of debtors was felt particularly when the stock of money in existence had substantially been absorbed by the usurers. There was little money to be had for payment of debts, and payment not forthcoming led to defaults; the debtor often entering into outright slavery to the creditor, or at least

all of his property reverting to the creditor’s possession. With defaults widespread, strong and broadly held sentiments brewed against the usurers, and spawned uprisings and revolutions. Thus, a finite supply of money made for a particularly volatile situation. With paper circulating as an exchange medium, the wealth of the land accrues to the usurers in exactly the same way, however, the usurer’s greed and covetousness does not mean quite so much danger to his life and limb, for paper offers him something that he did not have with gold, viz., control. Social unrest can be useful to professional usurers. But it is entirely useless if it cannot be controlled. If the absorption of wealth through usury threatens to reach levels that spawn social unrest, more paper can be printed and loaned into circulation to keep

_______________

A.R. Epperson, The Unseen Hand (Tuscon: Publius Press, 1985) p.132 133

the payments flowing and the spirits calm. When unrest benefits the cause of usurers (in order to keep an endless parade of baffling problems before the people, so that they continually appeal to “the government” for answers), all that need be done is to contract the supply of paper.

Unrest was useful to those who were striving for a complete monopoly on usury-generating paper in this country. The early American national banks did not provide all of the features they desired, but they provided enough for them to create the kind of financial crises that would keep the nation’s leaders searching for answers. After the charter of the Second National Bank expired, it also was not renewed. Strong popular opposition to the idea of a National Bank still existed,

thanks largely to the suffering and misery big banking had caused in its expropriation of wealth from the masses. As Epperson put it, “The Bank was using its powers to increase and decrease the money supply to cause, first inflation, and then deflation. This cycle was of benefit to the bankers who were able to repossess large quantities of property at a fraction of its real value.”

Andrew Jackson made the national bank an issue in his presidential campaign. That the popular sentiment in this country was set against the bank idea was indicated by the wide margin with which Jackson won the presidency. He was true to his campaign rhetoric, and in 1832 Jackson vetoed an act of Congress to re-Charter the national bank. For decades the nation was free of “legal tender” paper money and banking monopolies. As was noted. however, one way of stimulating the temptation for such things is the urgency of financing a war. There were a number of factors which contributed to the onset of America’s Civil War, and among them were economic issues, which tend to figure to some extent in all wars. Lincoln resisted the adoption of a national bank, but resorted to other measures that were little better to be esteemed in order to finance the war. One was an income tax, the first in our nation; another was bank chartering regulations, whereby a number of independent, paper-issuing banks could operate, rather than just one; and a third measure was the famous “greenback”, a U.S. Treasury Note which circulated as money. Debt accumulated rapidly, at usury, during the war. Government debt increased over 4000%, from $66.5 million to $2.67 billion between 1861 and 1865. Things in the private sector were not much better. Banks had to suspend the redemption of their paper. Many voices continued the cry for monetary reform. There eventually was the resumption of paper redemption, but it was at a discount that reflected the loss of value of the paper.

______________

IBID P.172

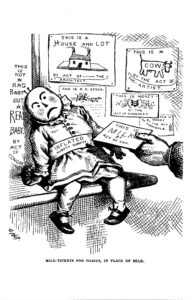

The proponents of a National Bank used every fiscal dissatisfaction and woe as an occasion to argue for the re-Chartering of the institution. Countering them were the tireless defenders of the silver and gold coinage for which the Constitution originally provided. A particularly entertaining example is an enlightening fable by David Wells titled Robinson Crusoe’s Money . Using the man-stranded-on-a-remote island theme, and building up from there, Wells enlightens the average

reader concerning the origins of economy and money, showing convincingly the follies of calling upon paper to fulfill the role of a valuable commodity, as a medium of exchange. Illustrations by Thomas Nast graphically portray monetary truths. One, which is included here, shows the ridiculousness of viewing paper as money itself rather than simply a claim to money.

The illusion of prosperity that attends the proliferation of bank paper proved to be tempting enough to endure the losses that attend the contraction of bank paper. America became addicted to paper, notwithstanding the “panics” that periodically ensued. Following the panic of 1907, President Roosevelt signed a bill creating the National Monetary Commission. As though the problem with the nation’s economy were a great mystery which never before had been addressed,

the Commission promptly went to Europe – the source of the problem – in search of answers. The American public was turning into the duped and intimidated body which it is today. They had become convinced that economics and monetary

______________

Originally published 1896, and reprinted by Greenwood Press New York, NY 1969

concerns were much too complex for the untrained mind, but that they need not worry, because the government’s panel of experts surely would come up with a solution. Of course, in Europe, the Commission learned all about the National Bank concept: a privately owned Bank, with an exclusive monopoly on usury reaping paper, which is declared by the government to be legal tender. Naturally,

this is the scheme which they were to propose. In 1910, the German Banker, Paul Warburg, held a secret meeting in which was drafted the legislation to accomplish this very thing. It became known as the “Aldrige Plan”, named after U.S. Senator Nelson Aldrige, who participated in the secret meeting. Strong opposition arose in Congress, and the plan failed ever to be considered for a vote. After elections, new support was gained for the measure. It was lightly gone over and re-submitted as new material, under a new name: The Federal Reserve Act. On December 23,

1913, with the thoughts of most of the nation fixed on Christmas, President Wilson signed it into law.

As an ideal, the Federal Reserve System closely approximated the goal of a monetary school that sometimes is called “social credit” or “monetary science”. In fact, one of this school’s learned advocates at the time, Senator Robert Owen, was a principal author of the original version of the Federal Reserve Act. Since this school of thought still enjoys a measure of popularity, it would be good at this point to glance at its basic position, and its idea of usury. A rudimentary concept of “monetary science” is that money is only a “token”. It is supposed to be a claim on the products and services of a society. This is a fundamental error, which

guarantees the fallaciousness of the entire system. In a free society, sellers are not compelled to sell. No one has a valid “claim” on any product based only on his possession of a piece of paper. The tyranny of “legal tender” laws is that if one chooses to sell something, then he must accept a certain type of paper in payment for it. Of course, if money is viewed as a claim ticket, then this suggests the obvious problem :who has the authority to issue such tickets?

Those of the “monetary science” school rightly were alarmed by the pretense of some bankers to create money out of nothing. What apparently had escaped their notice, however, was that the banker’s creation was not a claim ticket for existent products and services, but for non-existent silver and gold. They rightly analysed the potential for corruption in such a system; indeed such a system is corrupt in its very design. But their proposed solution aimed to cure the corruption in the

wrong way. They had no quarrel with the creation of money as such, but with who was creating it, and for what purpose. Their proposal was to take the money creation powers away from the bankers and give it to politicians! Gertrude M. Coogan, one of the early writers in this vein, states as an essential element of an “honest money” system: “The power to create money should be vested in a Monetary Trusteeship appointed by and answerable to the United States Congress. ” This is a classic case of putting the fox in charge of the chicken coop. It did not seem to occur to Miss Coogan, and others of this school, that ethically no one ought to be “creating” money – not the banks, nor the government.

A rudimentary principle of the American government is that rulers derive their just powers from the consent of the governed. That is, the interests which a legitimate government protects for society are the same which an individual would be justified in protecting for himself, e.g. defense, the guarding of property, etc. If an individual would like to enter into exchanges of property with others, it is necessary that he first produce something that he may contribute to such exchanges (even if this is only his labor). He would be totally unjustified in simply printing up

some paper that he declares to be a claim on the products of others. Of course, no one would take seriously any such claim. If one meant to press this sort of a claim, he probably would have to resort to intimidation or threat (legal tender laws), and any degree of success he had in thus acquiring the property of others would be considered extortion. If such a course is unthinkable for the individual, then how does it become thinkable for a “government”? How can a body of individuals delegate to a “government” a right and a power that none of them have as individuals?

Of course, legitimately they cannot. Frederic Bastiat enunciated this principle in a pamphlet titled “The Law”, first published in 1850:

The law is the organization of the natural right of lawful defense. It is the

substitution of a common force for individual forces. And this common force is

to do only what the individual forces have a natural a lawful right to do: to protect persons, liberties and properties; to maintain the right of each, and to cause justice to reign over all.

The “monetary science” writers would not do away with “money creation” in their proposal to strip the banks of these powers. They simply would transfer this power to the government. They were not concerned that the government would be less disciplined and more self serving than the banks in the role of “money creator”, because it was their vision to assemble a body of “Monetary Trustees” who had, in

______________

G.M. Coogan, Money Creators (1935; Hawthorn, CA: Omni, 1982), p.334

Declaration of Independence

F. Bastiat, The Law (1850; Irvington-on-Hudson, NY: FEE, 1984), p.7

the words of Rev. Denis Fahey, “an unblemished record for honesty and integrity. ”

Though it manifestly is a noble vision, it is a very shaky foundation for an “honest” money system. This also was what the “monetary scientists” hoped the Federal Reserve System would fulfill. They were bitterly disillusioned by the crash and depression of the 1930s. Miss Coogan published her book in 1935, and Senator Owen eagerly contributed a forward to it. In his comments, and by lending his name to Coogan’s book, Owen repudiated what the Federal Reserve turned out in

fact to be, as shall be discussed below.

The main problem with the Federal Reserve System, according the “monetary science” school, is that it consists mainly of privately owned banks that are allowed to create money out of nothing, which they lend out at usury. The “monetary science” proposal is that the government should create money and spend, not lend, it into circulation. Writers in this school rightly point out that as it is, newly created money is put into circulation only by way of a loan, but their alarm at this fact is misdirected. They observe that only the principal amount is created, and that

therefore not enough “money” exists to pay both the principal and interest. Rev. Denis Fahey has written, “The payment of the interest of money brought into existence as a debt involves the payment of more than is issued. This cannot be done without further borrowing, so the process means steady progression into debt for the society as a whole.” But this is true only if a “dollar” can be spent only once. In reality, there is a “velocity” of circulation of “money”, determined by the number of times it changes hands in a period of time. Given a high enough velocity, one “dollar” could pay all loans and usury. There is a practical limit to

velocity, such that usury eventually will become an arithmetic problem, however, it is not a good course to oppose usury only for the pragmatic reason of an arithmetic difficulty. Opposition to usury must have as its fundamental concern that usury is contrary to God’s law, and therefore is immoral. This is not the position expressed in the “monetary science” school. Consequently, it is not surprising to find these writers giving an inconsistent treatment of usury. Their problem with usury is only in case the principal was something which the lender created out of nothing. In the case of loans of existing assets, their system allows for usury. Miss Coogan, for instance, has said,

_______________

Rev. Denis Fahey, Money Manipulation and Social Order (1944; Hawthorne, CA: Ornni, 1986), p.69

IBID, p.36

“Note carefully that the original issuance or creation of money, paid into

circulation, should always be interest free. Carefully distinguish this original

issuance of money upon its creation with the lending of real money, which has

been obtained by those who have earned it by rendering personal services or

real goods in exchange for that money. In actually lending real money so

earned, one may expect a fair interest rate.

Thus, the “monetary science” position on usury is pragmatic in nature. They see usury as an evil only in such case as it ruins the monetary science system. Whereas they do not oppose usury on the basis of a principle of law, they accommodate usury in cases where their system would not require its censure. Their fixation with “paper money” is such that the evil and tyranny inherent in legal tender laws is ignored, for no “paper money” system can survive apart from some governmental power arbitrarily declaring some paper to be “money”. This is precisely what the Federal Reserve System is all about. The “monetary science” school is opposed to the Federal Reserve System not because its paper claims to money are fraudulent, but because it is the operation of private bankers.

The Federal Reserve System is a dream-come-true for the National Bank advocates. It created by law a “fractional reserve” national banking consortium. This provided an air of legitimacy to the centuries-old practice of keeping on hand only a fraction of the silver and gold which bank paper attests. The privilege of issuing this paper was granted to it by the government, and the government became its biggest customer, borrowing the paper on usury. This arrangement did not raise much protest because the Federal Reserve System was cleverly named so as to give the illusion that it was part of the government. It is not.

The Federal Reserve is a system of privately owned banks, whose affairs are directed by a Board of Governors, the chairman of which is appointed by the President. Though the Board technically has accountability to the government, in reality it acts independently of the government. The term of the Board Chairman is fourteen years, which hardly makes government control practical. The Board has broad powers of control. Their edicts dictate the extent to which the various member banks can create “money”. Economic analysts would have us believe that

mysterious factors influence the rates of price inflation and usury, but this

is mysterious only to those who are unacquainted with the powers of control that have been vested in the Federal Reserve System. Public outcry is stifled by this

________________

Coogan, Money Creators, p.1l8,119

shroud of mystery. The System never has been audited by a government agency, despite repeated requests by many influential members of government over the years. No other private corporation can boast of such an audit-free record.

Rather than one bank, the Federal Reserve is a system of twelve banks, each of which covers a region of the country. This gives the illusion of decentralization. All factors contributed to the confidence of the public, that the government finally was getting somewhere with the nation’s monetary troubles. This ill-conceived trust was so durable that it was not suspected that the two World Wars, and the crash and depression of the 1930’s had anything to do with banking shenanigans. Considerable evidence of this is available today, though it still is not popularly believed that the wars were planned, or that the depression was deliberately caused. Nevertheless, the culmination of their effects was public acceptance of the idea that more control over money was needed. By Executive Order, Roosevelt decreed that by May 1, 1933, all Americans had to surrender to Federal Reserve Banks, all gold coins and bars, and “Gold Certificates” (paper which entitled “the bearer” to a certain quantity of gold), in exchange for other currency. This was done “to provide relief in the existing national banking emergency, and for other purposes”, according to the Order. Americans by the millions lined up like sheep to comply with this lawlessness and tyranny. They thought it expedient to do so; the penalty for non-compliance was $10,000 (that is 1933 dollars) and/or 10 years imprisonment. Previously, even Federal Reserve notes were redeemable in gold. Following this order, a bank reserve in gold still was required, but gold was eliminated as a circulating medium. In 1965, in a revised coinage act, the government took away the silver also. They did not require that silver coins and “Silver Certificates” be surrendered. They merely stopped putting any silver into the coins that they minted, and rescinded the Silver Certificate’s promise of payment in silver on demand as of 1967. One still may spend silver coins today, though it is foolish to do so since they greatly exceed in value their copper/nickel look-alikes that have been dumped onto the market.

In 1971, President Nixon officially severed all remaining ties between the “dollar” and gold. The subtle redefinition of “dollar” had gone almost unnoticed by the public. The devious character of today’s “Federal Reserve notes” becomes evident in comparing the sets of “bills” on the following page. The old U.S. Treasury Silver Certificates were replaced with look-alike Federal Reserve notes, which make no reference to silver or redeem-ability. The Federal Reserve note clearly is modeled after the old silver certificate. Perhaps it was thought that the startling

changes in the nature of the paper might be concealed by the familiarity of a similar appearance. The serene gaze of George Washington is unchanged. But the representations of the paper are altogether different. No longer is there the commitment to pay anything on demand. The popular conception today is that the Federal Reserve note is a dollar. As there is neither expressed nor implied any “promise to pay”, it manifestly

is not a “note”, though it says Federal Reserve note. Though it says Federal Reserve note, there is nothing “Federal” about it. As was pointed out, the Federal Reserve Banks are privately owned corporations. The phrase “One Dollar” at the bottom is similar in appearance to the Silver Certificate, however, all of the fine print is missing. That being the case, the only interpretation that seems feasible is that this is a claim to be a “dollar”! This claim would have been met with either outrage or hilarity on the previous century.

What is more, paper and the printing press no longer are the preferred hardware of the inflationists/usurers. In the last quarter of the twentieth century, they use electronics. Federal Reserve notes still are printed, but they are issued only to meet the general public’s desire for currency. The quantity in circulation fluctuates with demand, rising during holidays, and then dropping off, and on the average it does not comprise any more than 30% of what the Federal Reserve now is calling “money”. In fact, a recent AP Wire Service report says that about $136 billion in Federal Reserve notes – 88% of the total in existence – is unaccounted for. Most of the “money” in circulation exists only as bank account balances – electronic impulses in banks’ computers. When checks are written on these accounts, mostly they are deposited by the payee. Account balances merely are credited or debited. Banking today is a giant clearing-house operation, with one important difference. The early clearing-houses kept their records on paper, and periodically paid off

balances in silver or gold. Today records are kept in electronic signals, and balances periodically are paid in paper.

The entire economy is “running on empty”. Earlier it was noted that the introduction of paper disrupted the concept of exchange, for when one receives paper, having given goods or services, the exchange is not complete until the paper is redeemed. The reality of the exchange was further muddled as men found ways of circulating the paper rather than redeeming it. In our time circulating paper is all that can be done with it. To think of “redemption” in connection with today’s “money” is nonsensical. Herrick said, “The large use of money and credits in modern times tends to obscure the fact that commerce is the giving of goods for

goods ” He wrote in 1920. Today it is evident that the use of paper and electronics not only “obscures the fact”, but destroys the reality of trading goods for goods. These things did not happen by way of natural evolution of economy, but were forced in this direction by men who desired to gain at the expense of others. Ludwig von Mises asserts,

Thus inflation becomes the most important psychological resource of any economic policy whose consequences have to be concealed; and so in this sense

it can be called an instrument of unpopular, that is, of antidemocratic, policy, since by misleading public opinion it makes possible the continued existence of a system of government that would have no hope of the consent of the people if the circumstances were clearly laid before them. That is the political function of inflation. It explains why inflation has always been an important resource of policies of war and revolution and why we also find it in the service of socialism.

In order for such an economic policy to survive, broad public confidence is required. Confidence is an inescapable part of the interrelations among men. In the ancient “natural economy” the required confidence was the confidence that one needed in his own productive abilities. In the “money economy”, a broader confidence was needed, but basically it was a trust that the man with whom one traded was not going to stab him in the back as soon as he turned to leave. The modern economy is by no means natural, and inasmuch as all true “money” has

____________

Herrick, p.9

Mises, A Theory of Money and Credit, p.255

disappeared, it cannot rightly be regarded as a “money economy” either, though generally it is held to be such. More accurately, it must be thought of as a “debt/credit” economy. The confidence that is required in order for such an economy to operate is not a confidence in oneself, or in fellow men, but in the paper and electronics that provide the illusion of wealth. Columnists Ross LaRoe and John Pool, writing in reference to the 1984 Ohio Savings & Loan crisis, said,

the recent problems, however temporary, of the savings and loan institutions in Ohio and Maryland have focused attention once again on the fragility of our monetary system. Although most of us don’t think much about it, the health of our whole financial system depends largely on our confidence in it. Like Tinkerbell, so long as we believe in it, it will work,

Professor Emeritus of Economics, James L. Green, University of

Georgia, put the same point in this way,

The recent “moritorium” in Ohio dramatized the fragile structure of our debt-based financial system. Depositors in Ohio lost confidence in the banking system and lined up to get their money. By the very act of withdrawing their money en masse, they forced the institutions to close their doors. Some 500,000 Ohioans were “locked out” with no access to their savings. Confidence melted away as fast as butter on a red hot stove.

Karen Horn, President of the Federal Reserve Bank of Cleveland, summed up the Ohio crisis in a way which Mr. and Mrs. Depositor should never forget. She stated succinctly: “Financial institutions really don’t run on cash as much as they run on confidence. There is no amount of cash delivery in the end that will do the trick if that confidence is stripped away.’,

Accordingly Mises has said, “… the circulation of fiduciary media [bank paper] is possible only on the assumption that the issuing bodies [The Federal Reserve Banks] enjoy the full confidence of the public, since even the dawning of mistrust would immediately lead to a collapse of the house of cards that comprises the credit circulation. ”

It is the usurer’s assets that are at risk in this “house of cards”, as well as the debtor’s. In fact, Mises, Sennholz, and others contend that usurers are at greater risk. Mises maintains, “The popularity of inflationism is in great part due to deep-rooted hatred of creditors. Inflation is considered just because it favors debtors at

______________

“The Columbus Dispatch”, Jan 21, 1986

Green, “The Disappearing Dollar”, April 14, 1985

Mises, A Theory of Money and Credit, p.397

the expense of creditors. ” Creditors are represented as at a disadvantage under inflation because loans are repaid with less valuable “dollars”. Even though usury would stipulate that a greater quantity of “dollars” be repaid than was loaned, still, the declining value of the “dollar” under inflation would eventually reach a point that the sum of what is repaid is worth less than the sum of what was loaned. But usurers should not be characterized as helpless in this situation. They have adjusted to these conditions in a number of ways. The “rate of interest” is adjusted in times of high inflation in order to compensate for declining “dollar” value. The term of loans is shortened so that “dollars” do not have as long a period of time over which to decline in value. And usury on mortgages no longer is “fixed”, but is made flexible, so as to respond to conditions that differ over time. Actually, usurers fare well in inflation. What they lose in unit value they make up in increased volume. Not only are the disadvantages of inflation effectively addressed by usurers, but there are a couple of advantages of inflation for usurers. The convenience of paper makes loaning easier, and the inflation of paper makes borrowing more necessary.

Also, the changes in the character of usury in this century would seem to favor the borrower. No longer do insolvent borrowers enter into slavery to their creditors. Bankruptcy laws have arisen to assure that usury takes on a more civilized appearance. Nor is the one in default liable to loose all of his property to the usurer, for the laws stipulate that certain types of property, such as tools of trade, cannot be confiscated. Yet usury must not be thought near extinction. These changes merely represent the changing tastes of usurers. Ancient usurers had a thirst for sheer power over other men. The process of foreclosure added wealth to

their coffers in the form of confiscated property and lives. Today’s usurers are more refined, and more future oriented in their perspective. They value the continued output of the little men, for the more the little men sweat, the more they line the usurer’s pockets. Today’s lust is for things. Whatever measures seem to benefit the borrowers will benefit the usurers even more, for it is from the sweat of the borrower’s brow that the things of the usurer eventually derive. A healthy, happy class of borrowers, who have the perception of security and the experience of confidence, will assure a steady flow of wealth into the hands of the usurers. If any should fall bankrupt, some property immediately reverts to the usurer, and any losses to the usurer are compensated by getting the borrower back onto his feet and paying loans and usury once again.

Another factor in the modern face of usury is that it may be found in every segment of society. The ancient stratification of society into the few usurers vs. the

_______________

Mises, Human Action, p.467

many borrowers proved to be dysfunctional because it was destablizing. War and revolution upset the lives of everyone. One way of helping this hazard of usury is the modern phenomenon of involving as many as possible in the lust for unjust gain. If more people have a vested interest in the continuation of the Tinkerbell system, that fact itself will keep it going longer. But an irrevocable principle of usury is that usury tends to concentrate wealth into the hands of the few. Even though there are numerous avenues today on which nearly everyone may dabble in

usury – and millions do – nevertheless a small fraction of “investors” have a corner on all those credit markets. One may think principally of the NOW accounts, Certificates of Deposit, Treasury Bills, Notes, and Bonds, Mutual Funds, and the like. Millions of petty usurers diminish their indebtedness by only a fraction by the meager gains they reap in their little “investments”. In reality, overall indebtedness continues to grow. The breakdown of confidence and the attending anti-social chaos will come eventually. Twentieth century professional usurers, who have greatly slowed the cycle of violence, hope that the future calamity may be deferred to the next generation.

A recent Washington Post story pictures one aspect of the current

problem in a graphic way:

Meet Ralph, the average American taxpayer who each year sends the government some of his paycheck to finance defense, national parks, Amrrack, education, welfare, subways, sewers, environmental protection and more.

Ralph probably doesn’t know it, but this year [1986] the government will take $699.23 of his $3,537 in federal income taxes to fund something that delivers no services at all. That is the payment of interest on the government’s unpaid debts.

These payments comprise the third largest item in the budget unveiled by

President Reagan, after Social Security and defense.

Usury now approaches 20% of the Federal budget, on a debt in excess of two. trillion “dollars” – that is 2,000,000,000,000. Part of the convenience of having a Federal Reserve System, which creates “money” out of nothing, is that if a debtor cannot repay his loan on time, it can be “refinanced” with the creation of additional “money”. In this way, usury payments continue to flow, though they continue also to mount. Debts, and usury, eventually mount up to a level that is even more impossible to pay. That precisely is the main problem in the “farm crisis” of the 1980s. Farmers by the thousands each year are losing their farms to banks because they cannot meet their debts. Their debts got to be as high as they were because they could not meet prior debts, which simply were refinanced. The source of all

________________

Appearing in “The Columbus Dispatch” Feb 16, 1986

the trouble is that their loans are loans upon usury. In addition to the Federal debt and the Farm debt, there is the Home Mortgage debt and Consumer debt of individuals, which amounts to another two trillion” dollars”, debts of business and industry amounting to 2.4 trillion, and the debts of state and local governments totaling 559 billion. This adds up to a grand total U.S. debt of over seven trillion

“dollars”.

One way of looking at this is the way in which the Washington Post article put it: “If Ralph earns $36,600, the median U.S. income for 1985, he has to work for 1 1/2 weeks this year just to pay the interest on the government’-s debt.” With private debt at the same level as Government debt, the average individual has to work another week and a half to pay the usury on the private debt. And then there is the debt of state and local governments. As it stands now, the average worker labors nearly a month out of every year to accomplish nothing but the payment of usury. Does America perceive herself as slowly but surely entering into indentured servitude? When will there be a general public outcry, as there was in ancient times? Will we need to be totally enslaved, working twelve months a year to pay usury?

E. L. Anderson has graphed the performance of the National Debt, Usury on the National Debt, the Consumer Price Index, and Federal Budget Deficits over the last several decades. These curves are reproduced on the following page. What is immediately apparent upon only a glance at these curves is that “something has got to give”. Though Anderson’s data is a bit old now, the situation has only worsened since 1979. His thesis is that the situation which these curves represent cannot continue, mainly because the line is converging on the vertical. Upon reaching vertical, time stops, which is an impossibility. What, however, is not an impossibility is that soon – no one can say how long it will take – usury payments will reach a critical threshold proportion of the Federal Budget, absorbing a critical threshold percentage of the Gross National Product, and the debt simply will be repudiated. As Mises said,

The Financial history of the last century shows a steady increase in the amount of public indebtedness. Nobody believes that the states will eternally drag the burden

_______________

Board of Governors of the Federal Reserve System, “Flow of Funds Accounts,

First Quarter 1986”, (Z.l June 1986, Flow of Funds, 1986:Ql), p.viii

E.L.Anderson, “The Upright Spike of ’79: Doomsday for America”, Washington: Government Education Foundation, 1978)

of these interest payments. It is obvious that sooner or later all these debts will be liquidated in some way or other, but certainly not by payment of interest and principal according to the terms of the contract.

One newsletter states that at the present rate of growth of government debt, usury on the debt will totally absorb our Gross National Product by 2013. It is much to be doubted that civilization will remain intact long enough for that to happen. That, of which Mises spoke in the ’50s, is upon us today. Foreign debt to American banks in many cases has become unpayable. Third World nations are threatening to repudiate this debt. This threat created what is already being called a “banking crisis“. A full range of tyrannical Executive Orders already are signed and waiting in the wings in the event of a “national emergency”. Remember what Roosevelt did in order to deal with “a national emergency in banking” Meanwhile, foreign debtors are enabled to maintain their usury payments by means of low-cost International Monetary Fund

_______________

Mises, Human Action, p.227

for more on the concealed tyranny of Presidential “Executive Orders”, see: Gary

North, Government By Emergency (FI. Worth: ABBR.), and F. Tupper Saucey, The Miracle On Main Street (Sewanee, TN:Spencer Judd)

loans. These loans are guaranteed by the U.S. Government. That means that if the foreign debtors do not pay, then the American taxpayers will pay. Either way the bankers will have their usury. When popular belief in Tinkerbell fails, professional usurers no longer will have any recourse for collecting debts. They are banking – literally – on the hope that widespread petty usury among the general population will provide enough popular incentive to keep the myth of Tinkerbell alive. This

actually amounts to a religious faith in the modern world that is not unlike the idolatry of ancient Babylonia. Now that so many are caught up in the web of usury, it will cost the average debtor a great deal to repudiate the mythology. There is a great vested interest to keep the “faith”, even though to an objective glance the ridiculousness of Tinkerbell is obvious.

The basic character of usury has not changed over the centuries. The idea of usury has evolved into highly complicated “interest theory“, but the function of usury, no matter what it is called, remains the same. Regardless of whether the loan is for business, or for meeting an urgent need; whether it is a loan of money, a loan of goods, or a loan of raw “purchasing power” in the form of paper or electronics, it remains unchanged that usury on the loan is gain to the usurer for which he did not labor, and is that for which the borrower did labor, but does not enjoy the benefit.

The modern face of usury is

1) the abstract nature of the loan principal; being in most cases that which a banker created by the stroke of his pen, and

2) the vast web of surety and petty usury into which the borrowing public has plunged. These developments highly complicate the matter, which complication hardly is to regarded as accidental. Now, it is only with difficulty that one can detect the hurt that usury is causing him.

And our culture is so secularized, and so self-centered, that virtually no one perceives nor cares that usury is causing great hurt to our nation as a whole.

Those who ought to occupy the City of God are for the most part welcoming the day of calamity, because they expect that its coming only signals the imminence of “the rapture”. However, in ever larger numbers, Christians are waking up to the fact that Christ is not the Lord of a defeated church. We must not desire escape, as though at last resort we would wish for the mountains to fall down and cover us. We have permitted the inhabitants of Babylon, the “earthly city”, to infest our land

even from its very foundation. For all that is right and true and glorious in our land, we never have had a truly righteous economy. The failure of our present unrighteous economy does not signal the imminent escape of the church, but the fall of Babylon. In order to establish righteousness in our midst, our first step is not to attempt to identify certain individuals or groups whom we feel are- responsible for our troubles. It is we who are responsible. The initial step of reform is repentance. We must show ourselves to be in truth God’s people, citizens of His City, by keeping His law, in His power and by His grace. There is no substitute for this.

The lessons of history are obscured, and we appear bound to re-learn them. Usury eventually and always destroys a nations economy. This appeared to happen more readily and more violently in the ancient world only because the ancient economies were not buffered with “money” that privileged men could create out of nothing. Once the commodities that were used in exchange were in sufficient measure absorbed by usurers, no recourse was left to the debtors but to choose slavery or revolution. Of the many iniquities that have plagued economies through the centuries, usury is the most destructive. Will we learn from history, or will we be forced to re-learn what ought to be crystal clear? One way or the other, the reality of the plague of usury shall become apparent. It is probable that the current economy has festered to the point that it cannot be reformed; it must be replaced. In that event we who are of the household of God ought not to pine for Babylon. For “the earthly city”, it is too late; but for the City of God, a new era of righteousness will have just begun.